Quad/Graphics (QUAD)·Q4 2025 Earnings Summary

Quad/Graphics Q4 2025: EPS In-Line, Revenue Slight Miss, 33% Dividend Hike

February 17, 2026 · by Fintool AI Agent

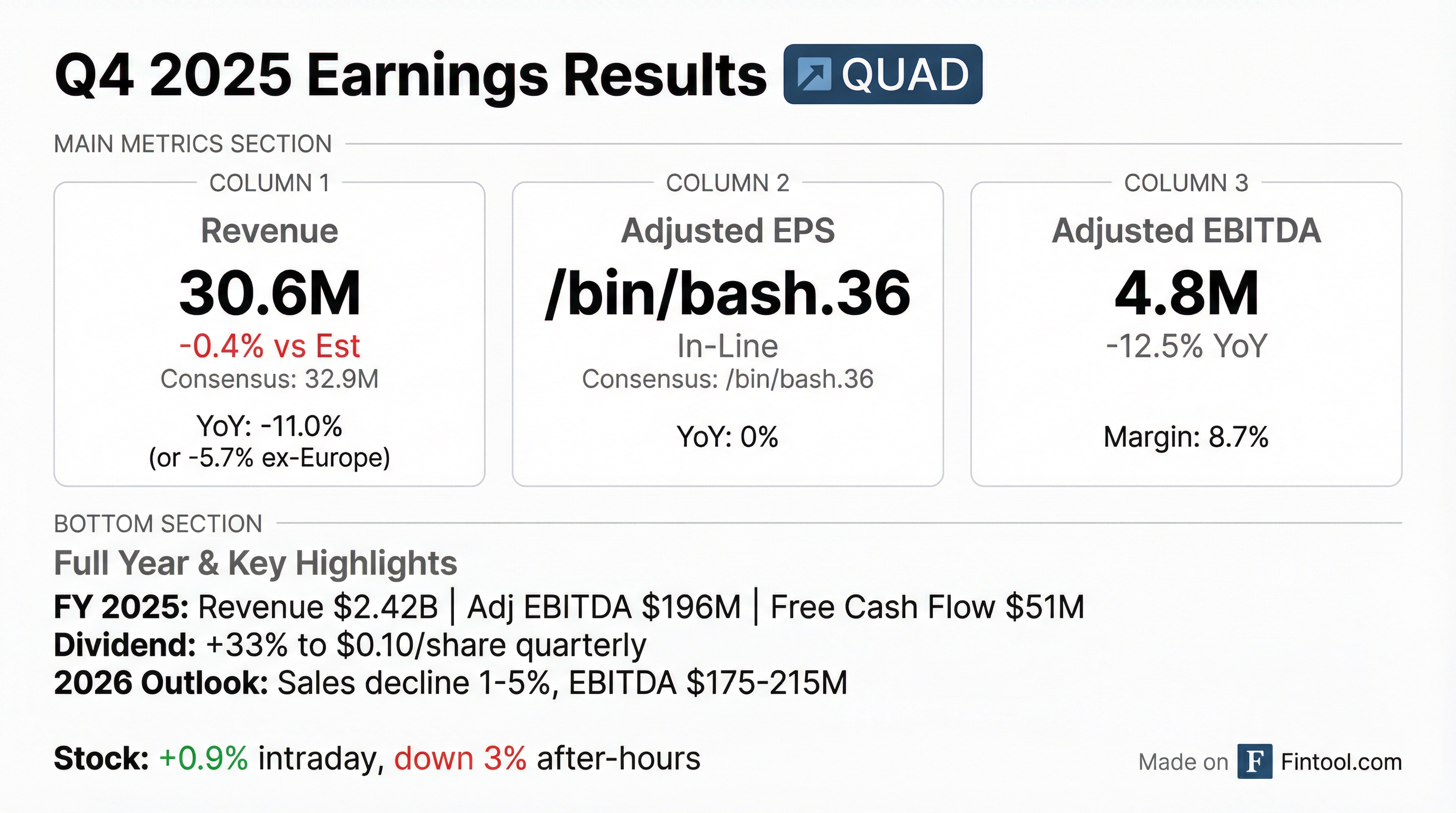

Quad/Graphics (NYSE: QUAD) reported Q4 2025 results that met adjusted EPS expectations while narrowly missing revenue estimates. The marketing experience company delivered adjusted EPS of $0.36 (in-line with consensus) on revenue of $630.6M, falling 0.4% short of the $632.9M estimate. The standout announcement was a 33% dividend increase to $0.10 per share quarterly, signaling management's confidence in the company's cash generation despite ongoing revenue headwinds.

Did Quad/Graphics Beat Earnings?

QUAD delivered in-line adjusted EPS and a slight revenue miss for Q4 2025:

The 11% headline revenue decline included a 5.3% impact from the Q1 2025 divestiture of European operations. Excluding this, core sales declined 5.7% driven by lower paper sales, reduced print volumes, and lower logistics sales.

Beat/miss context: QUAD has beaten EPS estimates in 3 of the last 4 quarters, with particularly strong surprises in Q1 2025 (+122%) and Q3 2025 (+15%).

How Did the Stock React?

QUAD shares traded up 0.9% during the regular session to $6.60, but fell 3% in after-hours trading to $6.40 as investors digested the mixed results and 2026 guidance.

The muted stock reaction reflects the market's focus on the trajectory rather than this quarter's numbers — QUAD is in a managed decline toward a 2028 growth inflection point.

What Did Management Guide?

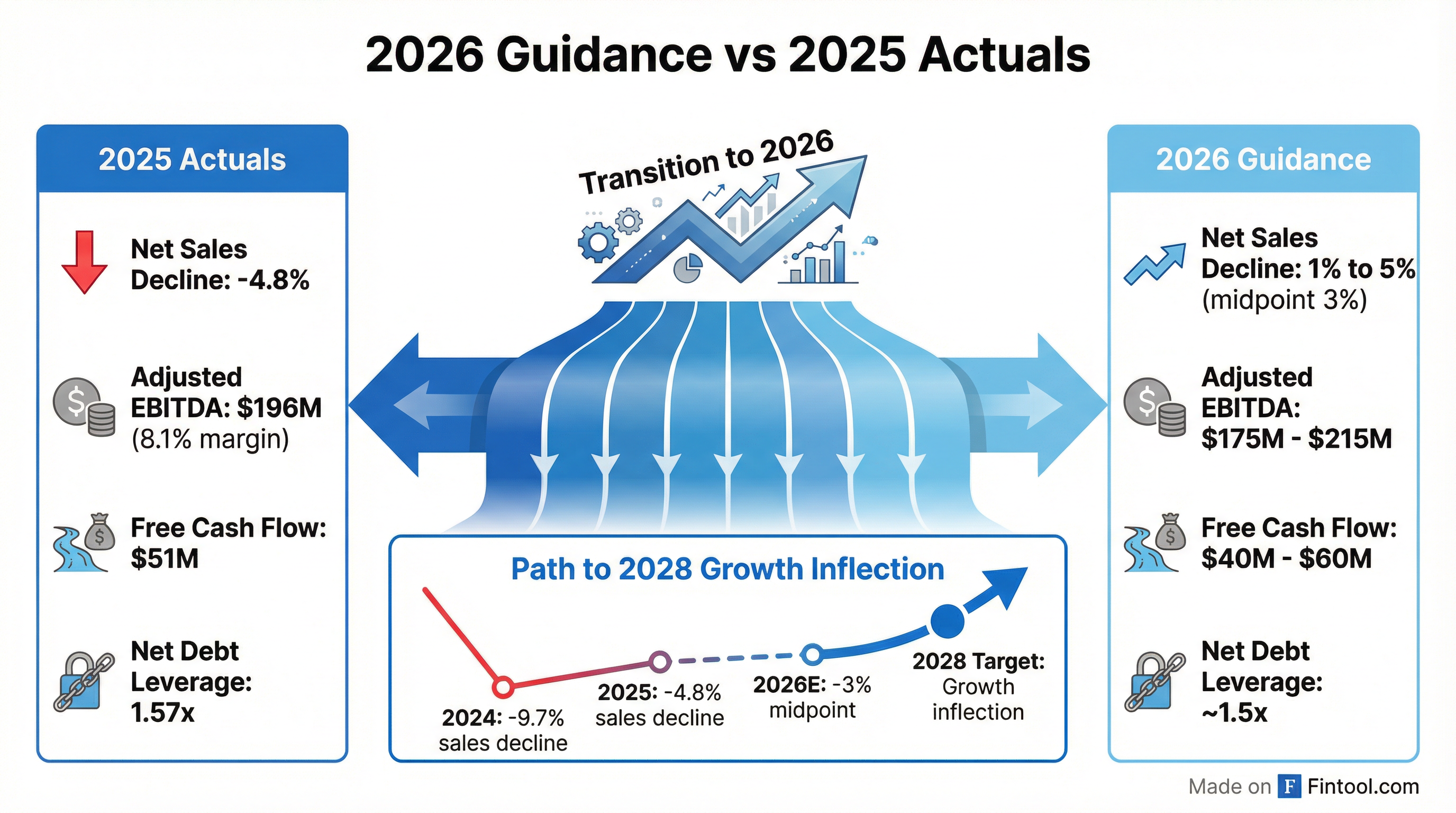

QUAD introduced 2026 guidance that shows continued progress toward sustainable growth:

The path to 2028: CFO Tony Staniak highlighted the improving trajectory — from 9.7% sales decline in 2024 to 4.8% in 2025 and now 3% at the midpoint of 2026 guidance. Management reiterated their target for a sales inflection to growth by 2028.

Long-Term Financial Goals:

What Changed From Last Quarter?

Improving profitability trends:

- GAAP net income swung to $27M profit in FY 2025 vs $51M loss in FY 2024

- Adjusted diluted EPS grew 19% YoY to $1.01

- Net debt reduced by $42M (12%) to $308M

Strategic progress:

- Completed integration of Enru's co-mail capabilities, expanding mail pool sizes and delivering higher postage savings

- Won new integrated creative and media work with Scandinavian Designs, Valvoline Instant Oil Change, and Gorilla Glue

- De-risked pension by annuitizing 32% of single-employer pension obligations ($96M liability), covering 6,200 participants (65% of total plan participants)

Revenue mix shift underway: CEO Joel Quadracci emphasized momentum in shifting revenue toward higher-value offerings including "Targeted Print" (direct mail, packaging, in-store) and integrated marketing services supported by data and technology capabilities.

Leadership Changes

QUAD announced two significant leadership structure changes designed to accelerate execution:

The leadership changes allow CEO Joel Quadracci to focus on long-term strategy, innovation, partnerships, and stakeholder relationships while Dave Honan drives operational execution.

MX Solutions Suite: Integrated Marketing Platform

QUAD's transformation centers on its MX Solutions Suite — an integrated set of marketing services designed to deliver end-to-end brand solutions:

Recent Client Wins:

- Heartland Dental: Deployed integrated data-backed direct mail strategy with pre-market testing and Quad's At-Home Connect for automated trigger-based programs

- Gorilla Glue Company: Betty and Rise agencies named creative and media agency of record for integrated campaigns across TV, digital, social, and out-of-home

- Pura: End-to-end in-store display support from concept development through distribution — their biggest in-store launch to date

AI Integration Across the Platform

QUAD highlighted AI implementations across all MX capabilities:

Capital Allocation: Dividend Takes Center Stage

The 33% dividend increase to $0.10/share quarterly ($0.40 annually) is the headline capital allocation move.

CFO Staniak noted the company expects to "remain opportunistic in terms of future share repurchases" while maintaining balance sheet strength with leverage near the low end of their 1.5x-2.0x target range.

Full-Year 2025 Performance

Segment Performance

The U.S. segment showed improved operating margins despite lower revenue, driven by manufacturing productivity gains and lower SG&A expenses.

Revenue Mix by Product Category (FY 2025 vs FY 2024):

The revenue mix shift toward higher-margin Targeted Print (up 100bps YoY) and away from declining Large Scale Print illustrates the transformation strategy in action.

Key Management Quotes

CEO Joel Quadracci on strategic momentum:

"We are gaining momentum in shifting our revenue mix toward higher-value offerings, including Targeted Print—such as direct mail, packaging and in-store—and integrated marketing services, supported by our data and technology capabilities. Strong demand for these solutions is driving larger, more strategic engagements with leading brands, which we believe will support sustainable long-term growth."

CFO Tony Staniak on the path to growth:

"Our Net Sales decline improved from 9.7% in 2024 to 4.8% in 2025 excluding the European divestiture, and in 2026 we anticipate further improvement to a decline of 3% at the midpoint of our guidance range."

Risks and Concerns

- Continued revenue decline: Even with improving trajectory, 2026 still projects 1-5% sales decline

- EBITDA pressure: Adjusted EBITDA guidance midpoint ($195M) is essentially flat YoY despite cost reduction efforts

- Secular headwinds: Traditional print volumes continue declining, requiring successful pivot to higher-value services

- Pension obligations: While de-risking has begun, pension liabilities remain on the balance sheet

- Tariff/trade exposure: Risk factors cite potential impacts from trade restrictions and currency fluctuations

Forward Catalysts

- Q1 2026 earnings (expected late April): First look at 2026 execution

- Marketing services wins: Pipeline of integrated creative and media deals with premier brands

- Postage savings: Enru integration delivering value to clients facing rising postal costs

- 2028 inflection progress: Continued monitoring of revenue decline trajectory

The Bottom Line

Quad/Graphics delivered a workmanlike quarter — meeting expectations while continuing to execute on its transformation strategy. The 33% dividend increase signals confidence in cash generation, while 2026 guidance suggests continued progress toward the 2028 growth inflection target. The stock's muted reaction reflects investor awareness that QUAD remains a "show me" story where each quarter's revenue decline improvement matters more than any single beat or miss.

For income-focused investors, the 6%+ dividend yield and improving leverage profile (1.57x, targeting 1.5x) may offer appeal. For growth investors, the transformation from legacy print to integrated marketing services remains early-innings with execution risk.

Next earnings: Q1 2026 expected late April 2026

View QUAD company profile | Read Q4 2025 earnings transcript